BDO Unibank has long been the crown jewel of Philippine banking—commanding scale, profitability, and a valuation premium that peers struggle to match. But its latest quarterly filing and sector trends suggest that the next chapter may be more challenging than the last.

The Margin Squeeze Begins

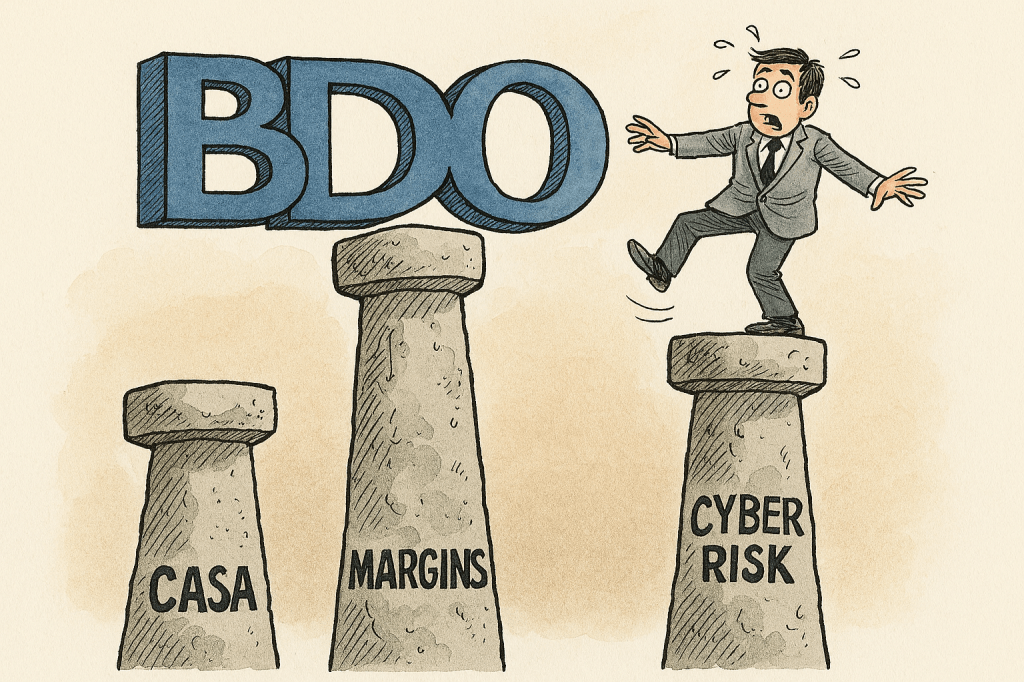

The first red flag is in the funding mix. Current and savings accounts (CASA)—the cheapest source of funds—slipped from about 71.5% at end-2024 to 66.6% by September 2025. Time deposits surged by nearly ₱300 billion. This isn’t just a footnote; it’s a structural shift that raises funding costs. Combine that with the Bangko Sentral ng Pilipinas’ rate-cut cycle—policy rate now at 4.75% and likely heading lower—and you have a classic margin squeeze: loan yields fall faster than deposit costs. For a bank with ₱5.27 trillion in assets, even a 10–20 basis point hit to net interest margin (NIM) can shave billions off earnings.

Consumer Credit: A Quiet Risk

BDO’s consumer book is growing, but so are its vulnerabilities. Credit card receivables past due beyond 90 days now hover around ₱20 billion—roughly 8% of the card portfolio. Restructured loans tell an even starker story: nearly 30% are overdue. These aren’t catastrophic numbers, but they hint at seasoning risk in unsecured lending, especially if economic growth cools. Sector analysts expect non-performing loans to inch up as banks chase retail growth. For BDO, that means higher provisions and a drag on profitability.

Costs Are Climbing

Operating expenses jumped 15% year-on-year, driven by branch expansion and technology upgrades. The bank plans to open 100–120 new branches, mostly in provincial areas—a strategic move to deepen reach. But until those branches deliver deposits and fee income, the cost-to-income ratio will feel the strain. Investors love growth stories, but they also watch operating leverage. Right now, that leverage is under pressure.

Cybersecurity: The Intangible Risk

A recent flap over unauthorized transactions reignited memories of past cyber incidents. BDO insists its systems are secure, blaming compromised client devices. Still, perception matters. In banking, trust is currency—and when trust wavers, valuation multiples can follow. The market doesn’t like uncertainty, especially in an era where digital channels dominate.

Valuation: The Premium Isn’t Guaranteed

BDO trades at a premium price-to-book ratio of around 1.3–1.4x, thanks to its scale and profitability. But if margins compress and costs bite, earnings growth could slow to single digits. That puts pressure on valuation multiples. A modest pullback—say 0.15x on P/B—could wipe out nearly ₱94 billion in market cap. Not a crash, but enough to make investors rethink lofty expectations.

The Offsetting Strengths

To be fair, BDO isn’t in trouble. Its capital buffers are strong (CET1 at 14.4%), provisioning is robust, and its franchise remains unmatched. Fee income is growing, and its bond market access gives it flexibility. But the message is clear: the premium isn’t automatic. CASA recovery, branch productivity, and credit discipline will decide whether BDO stays the market darling—or faces a valuation reset.

What to Watch

- CASA ratio: Can BDO claw back to 70%?

- NIM trajectory: How deep will the margin squeeze go as BSP cuts rates?

- Consumer credit: Will card and restructured loan delinquencies stabilize?

- Cost-to-income: Can new branches pay for themselves quickly?

- Cyber risk: Will BDO restore confidence after recent headlines?

Bottom line: BDO’s fundamentals remain strong, but the next 12 months will test its ability to defend its premium. For investors, this is no time for complacency.